Life insurance products come in many variations, each catering to different needs and goals.

Term Life Insurance stands out as a fundamental protection product, offering essential coverage for life’s uncertainties.

In this comprehensive guide, we delve into the intricacies of Term Plans, what they are, why you need them, and how to choose the right one for you.

Types of Life Insurance

- ULIP (Unit Linked Insurance Plan): A blend of investment and insurance.

- Whole Life Insurance: Provides coverage for the insured’s entire lifetime.

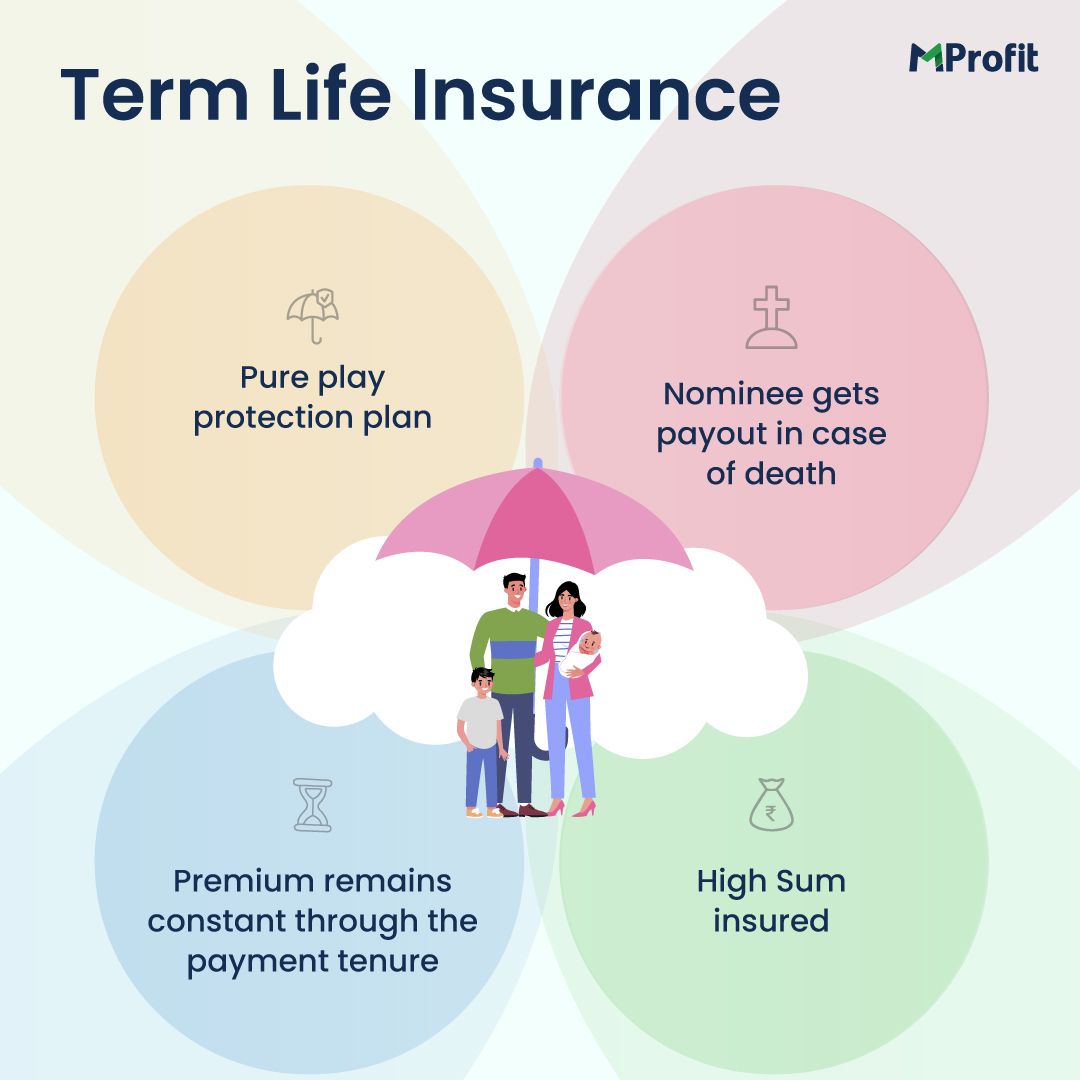

- Term Life Insurance: A pure protection policy offering high coverage at low premiums.

Among these, Term Life Insurance is the most straightforward and crucial form of life insurance.

It ensures your family’s financial stability by providing a substantial sum assured in exchange for affordable premiums.

What is Life Insurance?

A Life Insurance policy provides financial security to the family of the insured in case of the insured person’s death during the policy period.

In some cases, it also provides a maturity benefit to the insured person after a set period.

Types of Life Insurance

Life insurance policies can be categorized into two main types:

- Savings Policies: These policies offer a combination of insurance and investment benefits.

- Protection Policies: These policies only provide life insurance coverage.

Savings Policies

Savings policies come in different forms, each offering a mix of insurance and investment opportunities. They include:

- Unit Linked Insurance Policies (ULIPs)

- Non-Linked Participating Plans

- Non-Linked Non-Participating Plans

Pure Play Protection Policies

Pure play protection policies focus solely on providing life insurance coverage without any investment component.

What is Term Insurance?

Term Insurance is a type of life insurance that provides coverage for a specified term.

If the insured person passes away during this term, the policy pays out a death benefit to the beneficiaries.

Term insurance does not include any investment component or maturity benefit.

Example of a Term Insurance Cover

Do You Need Life Insurance?

Deciding whether you need life insurance depends on your individual circumstances.

Life insurance can provide financial security for your dependents in the event of your untimely death.

How Much Cover Is Required for a Life Insurance?

When selecting a life insurance policy, consider the following factors to determine the appropriate coverage amount:

- Income: Ensure that the coverage amount can replace your income for a certain period.

- Expenses: Include daily living expenses, education costs, and other recurring expenses.

- Assets: Consider your existing assets and how they can be used to support your family.

- Liabilities: Account for any debts or liabilities that need to be paid off.

At What Age Should You Buy a Term Plan?

There is no specific age to buy a term plan, but purchasing it early can be beneficial.

Younger individuals typically get lower premium rates, making it cost-effective in the long run.

Conclusion

Term Life Insurance is a vital component of financial planning, providing essential protection for your loved ones.

By understanding the basics of life insurance and considering your individual needs, you can make an informed decision about the right policy for you.

*Disclaimer – This is for information purposes only and not investment advice. Data credit to the rightful source.

Comments